As Nepal steps into the new fiscal year 2081/82, significant changes have been introduced (while others are following up soon) in the financial transaction landscape, particularly in the digital payments. Now, let’s imagine a bustling market in Nepal, where traders and customers have adopted the convenience of digital wallets and online payment systems. But now, a new twist emerges in the story – paying digitally comes with a fee, while cash remains free.

The Finance Ordinance 2081 has brought a significant shift: the application of VAT on digital payment transactions via ConnectIPS, and new transaction fees for digital wallet users. These changes, while intended to increase government revenue, have sparked a debate about their impact on the adoption of digital payments. As the plot become set/known wider, we see the implications unfold, affecting individuals and businesses alike.

In this article, we explores the implications of these changes, compare them with global practices, and discuss potential impacts on consumers and businesses in Nepal.

Introduction of VAT on payment transactions via ConnectIPS

ConnectIPS, a popular payment system in Nepal, has started charging Value Added Tax (VAT) on its transaction fees as per the Finance Ordinance 2081. Previously exempt from VAT, Clearing House Services have been delisted from the VAT exemption list, making all associated fees subject to an additional 13% VAT.

- Previous Fee Structure (Highest for standard transaction): NPR 8 per transaction

- New Fee Structure: NPR 8 + 13% VAT = NPR 9.04 per transaction

This change is significant as it increases the cost of each transaction, affecting both individual users and businesses relying on ConnectIPS for payments. As per the latest annual report published by NRB which is of 2022-23, which includes the user count for ConnectIPS which shows that is at 11,08,436 as of mid-July, 2023. So, even a small change makes a huge difference when the transaction counts are huge from these users on day to day basis.

Changes in Digital Wallet Transactions

In a similar way, eSewa, a leading digital wallet in Nepal, has introduced new transaction fees. The post itself was circulated and removed within hours from their social media channel. This is how the post looked like:

The post even if removed was already indexed along with their older posts in google search as well (different story as they do not open the following post as it’s removed) :

The notice was later re-published with a slight change in color and most of the text in the caption removed. With this change, effective from today – August 1, 2024, eSewa is now charging a fee for peer-to-peer (P2P) money transfers beyond a certain limit:

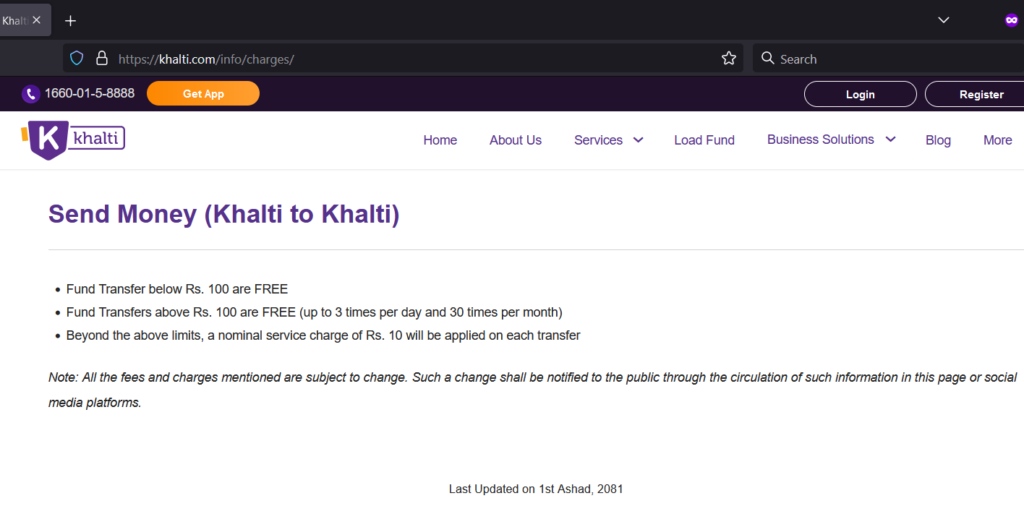

- Free Transactions: Up to 3 transactions per day and a total of 30 transactions per month (averaging out at 1/day).

- Chargeable Transactions: NPR 10 per transaction for any amount exceeding NPR 100 beyond the free limit.

- Transactions below NPR 100 remain free even after 3/day or 30/month transaction limit.

This move aims to regulate the frequency of transactions and ensure the sustainability of the service while contributing to their own revenue. There are currently 1,89,41,793 registered wallet users (as of Mid-July, 2023 per NRB report) in Nepal which is set to impact many of these users.

Another wallet provider in Khalti did follow through the same path enforcing the same limits. They did post the announcement and made amends on 17th Shrawan, 2081 – however, their website page falsely claims to have made the update on 1st Ashad, 2081 – with their website stating “Last Updated on 1st Ashad, 2081” in the last line as we can see in the screenshot below:

Critique: Discouraging Digital Service Usage

These practices are on the wrong direction, discouraging users from making use of digital services when these services should rather be promoted. The additional charges and VAT could lead users to revert to cash transactions to avoid extra costs, counteracting efforts to create a cashless economy.

Global Comparisons: Transaction Fees and Rebates

While Nepal is increasing the cost of digital transactions through VAT and service fees, some countries have adopted different approaches, offering rebates and incentives to promote digital payments.

1. India India has implemented a series of measures to promote digital transactions, including no VAT or additional transaction fees for users; cashback schemes and incentives for merchants who accept digital payments. For instance, the Indian government introduced the “Lucky Grahak Yojana” and “Digi-Dhan Vyapar Yojana” which offered cash rewards to consumers and merchants using digital payments.

The cashback schemes under “Lucky Grahak Yojana” and “Digi-Dhan Vyapar Yojana” reported distributing over INR 1 billion in rewards within the first few months of implementation.

2. China In China, digital payment platforms like Alipay and WeChat Pay often provide users with discounts and rebates on transactions to encourage usage. These incentives have significantly contributed to the widespread adoption of digital payments across the country with Alipay and WeChat together reaching to over 1 billion user base.

3. United States In the United States, credit card companies frequently offer cashback and rewards programs to encourage the use of digital payments. There’s obviously no VAT charged on transaction fee but rather they enforce incentives, ranging from 1% to 5% cashback on purchases. This has helped make digital transactions more attractive to consumers and the standard go-to, with an estimated 77% of credit card users participating in rewards programs.

Implications for Nepal

The introduction of VAT and transaction fees in Nepal is likely to have several implications:

- Increased Cost for Users: The additional charges could discourage frequent small transactions, particularly affecting low-income users who rely on digital payments for daily transactions.

- Impact on Digital Payment Adoption: While the fees might increase revenue, they could also slow down the adoption of digital payments if users revert to cash transactions to avoid extra costs.

- Revenue Generation: The government aims to increase its revenue through these charges, which can be used to fund public services and infrastructure projects.

सरकारले यी शुल्कहरूको माध्यमबाट आफ्नो राजस्व वृद्धि गर्न खोजेको छ, जुन सार्वजनिक सेवाहरू र पूर्वाधार परियोजनाहरूमा प्रयोग गर्न सकिन्छ। अर्थात्, हामी सबैलाई थप शुल्क तिरेर बबाल बाटो, पुल, र सरकारी कार्यालयको सुविधा दिने सौभाग्य प्राप्त हुने भएको छ।

Referencing Satirical statement shared by a user

The fiscal changes in Nepal’s digital payment landscape reflect a wider pattern of government seeking to generate revenue from the people – with recent changes around added extra tax for fuel charges as well. While these changes aim to ensure sustainability and increase government revenue, it is essential to balance them with incentives to promote digital payment adoption. Learning from global practices, Nepal could consider introducing cashback schemes or rebates alongside transaction fees to encourage continued use of digital payment systems. This approach would ensure a steady revenue stream while fostering a cashless economy and enhancing financial inclusion.